Schedule your free consultation today and discover how dental implants can change your life.

Step-by-Step: How to Get a Dental Implant Loan

The process is more straightforward than most patients expect. Here's the typical path:

Get a treatment plan with a precise cost from your dental provider

Estimate insurance and HSA contributions to determine the amount needing financing

Pre-qualify with multiple lenders using soft credit checks

Compare offers — APR, term, fees, monthly payment

Submit a formal application for the best option

Lender pays the practice directly for the treatment

Make monthly payments to the lender over the loan term

Total time from application to funded: typically 1–3 days for healthcare lenders, 1–2 weeks for traditional banks.

Where to Get Dental Implant Loans

1. Healthcare-specific lenders

Specialized lenders for medical and dental procedures:

Cherry

$200–$10,000 typical loan range

0–35% APR depending on credit

3–60 month terms

Soft credit check for pre-qualification

Some 0% promotional offers for short terms

Sunbit

Up to $10,000

6–24 month terms

Soft credit check

Quick decisions

Best for smaller cases

Proceed Finance

Up to $50,000+

24–84 month terms

Larger case specialty

Soft credit check for pre-qualification

Better rates for stronger credit

LendingClub Patient Solutions

$1,000–$50,000

24–84 month terms

Hard credit check at application

Competitive rates for good credit

Prosper Healthcare Lending

Marketplace approach

Multiple lender offers from one application

Up to $100,000 for large cases

2. Healthcare credit cards

CareCredit

Most widely accepted at dental practices

Promotional 0% periods (6, 12, 18, 24 months)

Standard APR 14.9–17.9% after promotional period

Deferred interest — if not paid in full during the promotional period, interest is calculated retroactively

Hard credit check

Wells Fargo Health Advantage

Similar concept to CareCredit

Comparable terms

Best for: patients who can confidently pay off within the promotional window.

3. Personal loans from banks and online lenders

For patients with good credit, traditional personal loans often offer the lowest rates:

SoFi — 8–35% APR, no fees, $5,000–$100,000

LightStream — 8–25% APR, no fees, $5,000–$100,000

Marcus by Goldman Sachs — 7–25% APR, no fees, $3,500–$40,000

Discover Personal Loans — 7–25% APR, no fees, $2,500–$40,000

Local credit unions — often lowest rates for members

Best for: good-to-excellent credit, larger amounts, lowest total cost.

4. Home equity loans and HELOCs

If you own a home with equity:

Lower interest rates than unsecured loans (typically 7–10%)

Larger amounts available

Interest may be tax-deductible for medical use (consult your tax advisor)

Slower approval (2–6 weeks)

Secured by your home — defaulting risks foreclosure

Best for: large cases ($30,000+), homeowners with equity, patients with discipline to make payments.

5. 401(k) loans

Some retirement plans allow loans:

Borrow from your own retirement funds

Repay yourself with interest

5-year repayment typical

No credit check

Risk: if you leave your job, the loan may need to be repaid quickly

Risk: opportunity cost of removing money from retirement

Best for: patients who maximize their 401(k) and have little credit access.

6. In-house payment plans

Many practices offer financing without involving third parties.

Decisions in a single visit

Often no credit check for smaller amounts

Flexible terms

Direct relationship with practice

Lower amounts than third-party loans typically

Best for: most patients as a starting point, especially those with credit concerns.

Good care keeps implants healthy for decades

How to Get Pre-Qualified

Pre-qualification gives you loan offers without affecting your credit. Steps:

1. Gather basic information

Your full name, address, date of birth

Social Security number (for soft credit pull)

Annual income

Monthly housing payment

Employment information

2. Visit the lender's website

Most healthcare lenders have a "pre-qualify" or "check rate" link. This uses a soft credit check.

3. Enter the requested loan amount

Pre-qualify for the amount your treatment plan requires.

4. Receive offers within minutes

You'll see APR, term, monthly payment, and total cost.

5. Compare multiple offers

Pre-qualify with 3–5 lenders to compare. Soft pulls don't accumulate to hurt your credit.

6. Apply formally for the best option

Once you choose, submit a formal application. This typically involves a hard credit pull and detailed verification.

How Much Can You Borrow?

Loan amounts depend on your credit, income, and existing debt:

Credit Profile

Typical Maximum

Excellent (740+)

$50,000–$100,000

Good (700–739)

$25,000–$50,000

Fair (640–699)

$10,000–$25,000

Poor (580–639)

$2,000–$10,000

Bad (under 580)

$500–$5,000 (specialty lenders)

These are general ranges. Income and existing debt also matter.

What Lenders Evaluate

Beyond credit score:

1. Debt-to-income ratio

Total monthly debt payments divided by monthly income. Most lenders want under 40%.

2. Income stability

Steady employment 1–2 years preferred. Self-employment requires more documentation.

3. Length of credit history

Longer history with good payment record is favorable.

4. Recent credit applications

Many recent applications can lower approval odds.

5. Existing debt

High balances on other loans or credit cards reduce capacity.

6. Banking history

Active checking account in good standing.

Improving Your Approval Odds

Before applying:

1. Check your credit reports

Get free reports from AnnualCreditReport.com

Dispute any errors

Verify the information lenders will see

2. Pay down credit card balances

Even temporary paydowns can improve your score before applying.

3. Avoid new credit applications

Each hard pull lowers your score temporarily. Save credit applications for the loan you actually want.

4. Increase your reported income

Update your employer information

Document side income or self-employment

Include any government benefits

5. Consider a co-signer

A co-signer with strong credit dramatically improves approval and reduces interest rates.

6. Reduce existing debt

Paying down other loans before applying improves debt-to-income ratio.

Comparing Loan Offers

When you have multiple offers, compare:

Total cost over the loan

Multiply monthly payment by number of months. The cheapest monthly payment isn't always the cheapest total cost.

APR (not just interest rate)

APR includes fees and gives a true comparison between lenders.

Term length

Shorter terms = lower total cost but higher monthly payments.

Fees

Origination fees (typically 0–10%)

Late payment fees

Prepayment penalties (avoid if possible)

Flexibility

Can you change due dates?

Can you skip a payment in hardship?

Can you pay off early without penalty?

Lender reputation

Customer reviews

Better Business Bureau rating

Years in business

Regular checkups protect your investment

Common Mistakes to Avoid

1. Focusing only on monthly payment

Long terms with low monthly payments often cost much more in total interest.

2. Accepting the first offer

Pre-qualifying with multiple lenders takes minutes and can save thousands.

3. Ignoring deferred interest

Promotional 0% offers often have deferred interest that applies retroactively.

4. Borrowing more than needed

Some lenders push higher amounts. Borrow only what your treatment costs.

5. Underestimating insurance

Get a precise insurance estimate before financing. You may need less than expected.

6. Skipping the pre-qualification step

Going straight to a hard credit pull lowers your score unnecessarily.

7. Missing the truth-in-lending disclosure

This document shows total cost, APR, and all fees. Always read it.

What If You're Denied?

Denial doesn't end your options:

1. Apply elsewhere

Different lenders have different criteria. A denial from one doesn't mean denial from all.

2. Apply with a co-signer

The single most effective way to gain approval.

3. Try in-house payment plans

Practices have flexibility that third-party lenders don't.

4. Reduce the loan amount needed

Use HSA/FSA savings

Maximize insurance benefits

Stage treatment over time

Choose less expensive options

5. Improve credit and reapply

6–12 months of focused improvement can change your options

Pay down debt

Establish positive payment history

Check for and dispute errors

6. Wait for better offers

Lender terms change. Check back periodically.

Frequently Asked Questions

How long does it take to get a dental implant loan?

Healthcare lenders: minutes to days. Personal loans: days to weeks. Bank loans and HELOCs: 2–6 weeks.

Will applying for a loan affect my credit score?

Pre-qualification (soft pull): no impact. Formal application (hard pull): typically 5–10 point temporary drop.

Can I get a loan for the full cost?

For most cases yes — depending on credit and income. Larger cases may require a down payment or co-signer.

Should I use savings or get a loan?

Depends on your interest rate and savings rate. If your loan rate is lower than your investment returns, it may make sense to finance and keep savings invested. If loan rates are high, paying cash is often better.

Can I use multiple loans for one treatment?

Yes — patients sometimes combine in-house plans with healthcare loans, or use HSA savings plus financing. Combining can optimize total cost.

What if I lose my job during repayment?

Contact the lender immediately. Most have hardship programs. Don't miss payments without communicating.

Ready to plan your treatment financing?Schedule a consultation — we'll provide a precise treatment plan, help you understand financing options, and connect you with the right lenders for your situation.

As Northern California's leading dental implant center, we combine advanced surgical expertise with compassionate patient care to deliver life-changing smile transformations. Every procedure is performed by board-certified oral and maxillofacial surgeons using state-of-the-art 3D imaging and guided surgery technology.

Board-Certified Oral Surgeons

Our surgeons are board-certified by the American Board of Oral and Maxillofacial Surgery, ensuring the highest standard of training and expertise in dental implant placement, bone grafting, and full-arch restoration procedures.

Lifetime Warranty on Full Arch Prosthetics

We back our full-arch zirconia prosthetics with a lifetime structural warranty. If a prosthesis cracks or breaks under normal use, we replace it at no cost. Our in-house dental laboratory crafts each prosthetic with premium materials.

Unlike most practices that outsource lab work, Fusion Dental Implants operates its own on-site dental laboratory. This means faster turnaround times, precise custom-fitted restorations, and same-day teeth solutions for qualifying patients.

Price-Match Guarantee

We believe premium dental implant care should be accessible. Our price-match guarantee means if you receive a lower quote from a qualified provider for the same procedure, we will match or beat that price while maintaining our exceptional quality standards.

About Us

About Fusion Dental Implants

With over 18 years of experience and a team of the best board-certified oral and maxillofacial surgeons, Fusion Dental Implants is dedicated to providing the highest quality dental implant care in Northern California.

Our practice specializes in full-arch dental implant solutions including All-on-4 and All-on-6 procedures, single tooth implants, implant-supported dentures, and complex bone grafting cases.

With four convenient locations in Roseville, El Dorado Hills, Folsom, and Rocklin, we serve patients throughout the Sacramento metropolitan area, Placer County, El Dorado County, and the greater Northern California region.

Our state-of-the-art facilities feature cone beam CT scanning, digital treatment planning, and an in-house dental laboratory that enables same-day teeth procedures.

We understand that dental implants are a significant investment in your health and quality of life. That is why we offer flexible financing — single-tooth implants from $60/month, All-on-4 full arch from $250/month — accept most major dental insurance plans, and provide a price-match guarantee.

Every patient receives a complimentary consultation with a comprehensive treatment plan tailored to their specific needs and budget.

FAQ

Frequently Asked Questions

Find answers to the most common questions about dental implants, our procedures, costs, and what to expect at Fusion Dental Implants. Still have questions? Contact us for a free consultation.

How much do dental implants cost at Fusion Dental Implants?

Dental implant costs vary based on the type of restoration needed. Single tooth implants start at approximately $1,850, implant-supported dentures begin around $9,999, and full-arch All-on-4 solutions start at $17,999 per arch.

We offer a price-match guarantee and flexible monthly financing — single tooth from $60/month, full arch from $250/month. During your free consultation, we provide a detailed treatment plan with transparent pricing and no hidden fees.

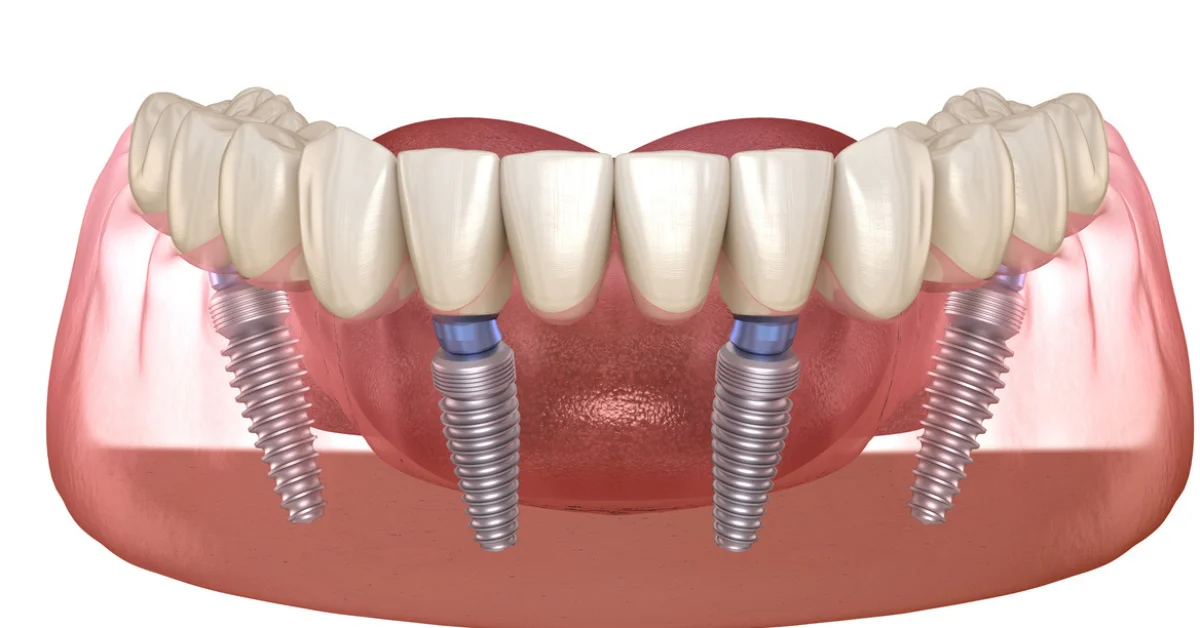

What is the All-on-4 dental implant procedure?

All-on-4 is a revolutionary full-arch dental implant technique that replaces an entire arch of teeth using just four strategically placed titanium implants. The procedure is designed so that patients can receive a complete set of fixed, non-removable teeth in a single day.

Two implants are placed vertically in the front of the jaw and two are angled at up to 45 degrees in the back, maximizing bone contact and often eliminating the need for bone grafting.

At Fusion Dental Implants, our board-certified oral surgeons have performed thousands of successful All-on-4 procedures.

How long do dental implants last?

With proper care and maintenance, dental implants can last a lifetime. The titanium implant post that is surgically placed into the jawbone integrates with the bone through a process called osseointegration, creating a permanent foundation.

The implant crown or prosthetic typically lasts 15 to 25 years before it may need replacement due to normal wear.

At Fusion Dental Implants, we use premium zirconia restorations, with our full-arch zirconia prosthetics backed by a lifetime structural warranty, and our in-house lab ensures each restoration is crafted for maximum durability and aesthetics.

Am I a candidate for dental implants?

Most adults with good general health are candidates for dental implants. During your complimentary consultation, our surgeons evaluate your jawbone density using advanced 3D cone beam CT imaging, review your medical history, and assess your oral health.

Even patients who have been told they do not have enough bone for implants may be candidates through bone grafting procedures, zygomatic implants, or the All-on-4 technique which utilizes existing bone more efficiently.

Conditions like diabetes, smoking, and osteoporosis require special consideration but do not automatically disqualify you.

What is the recovery time after dental implant surgery?

Recovery varies depending on the complexity of the procedure. For single implant placement, most patients return to normal activities within one to two days, with mild soreness lasting three to five days.

For full-arch procedures like All-on-4, patients typically experience moderate swelling for three to five days and are comfortable enough to eat soft foods the same day they receive their temporary teeth.

Full osseointegration, where the implant fuses with the jawbone, takes three to six months, during which you wear a functional temporary restoration.

Do you offer financing for dental implants?

Yes, we offer several flexible financing options to make dental implants affordable. Our monthly payment plans start as low as $60/month for single-tooth implants, $150/month for implant-supported dentures, and $250/month for All-on-4 full-arch restorations.

We partner with leading healthcare financing companies to offer plans with competitive interest rates and terms up to 84 months. We also accept most major dental insurance plans, including PPO plans, and our team helps maximize your insurance benefits.

Every patient receives a clear breakdown of costs during their free consultation.

What makes Fusion Dental Implants different from other providers?

Several factors set Fusion Dental Implants apart. Our practice is led by board-certified oral and maxillofacial surgeons with specialized training in implantology.

We operate our own in-house dental laboratory, which allows us to provide same-day teeth and ensures the highest quality custom restorations. Our lifetime warranty on full-arch zirconia prosthetics demonstrates our confidence in our work.

We offer a price-match guarantee, and our four convenient Northern California locations in Roseville, El Dorado Hills, Folsom, and Rocklin make access easy for patients throughout the region.

What are the advantages of dental implants over dentures?

Dental implants offer several significant advantages over traditional removable dentures. Implants are permanently fixed in place, so they do not slip, click, or require adhesive.

They preserve jawbone density by stimulating the bone just like natural tooth roots, preventing the facial collapse and bone loss that occurs with dentures over time. Implant patients can eat all their favorite foods without restriction, speak clearly without worry, and smile with confidence.

While the initial investment is higher than dentures, implants are more cost-effective long-term because they do not need to be replaced every five to seven years like dentures typically do.

Have a question that is not answered here? Our team is ready to help.

Dental implants have transformed modern dentistry, offering a permanent solution for missing teeth that looks, feels, and functions like your natural smile. Explore the topics below to learn how implants work, what materials we use, and how to plan your treatment with confidence.

Types of Dental Implants Explained

Dental implants come in several varieties designed to address different clinical needs.

Endosteal implants are the most common type and are placed directly into the jawbone, typically made from biocompatible titanium that fuses with your natural bone over three to six months through a process called osseointegration.

These implants serve as artificial tooth roots and can support single crowns, bridges, or full-arch prosthetics depending on how many teeth need replacement.

For patients who lack sufficient bone height in the upper jaw, zygomatic implants offer an advanced alternative. These longer implants anchor into the dense cheekbone (zygoma) rather than the maxilla, eliminating the need for bone grafting procedures that can add months to treatment timelines.

At Fusion Dental Implants, our oral surgeons have extensive training in zygomatic implant placement, making this option available to patients who have been told they are not candidates for traditional implants.

Subperiosteal implants rest on top of the jawbone beneath the gum tissue rather than being embedded within the bone. While less common today due to advances in bone grafting technology, they remain an option for patients with significant bone loss who prefer to avoid grafting.

Mini dental implants, which are smaller in diameter than standard implants, are often used to stabilize lower dentures or in areas with limited bone width.

Your surgeon will recommend the implant type best suited to your specific anatomy, bone density, and treatment goals during your comprehensive consultation.

The Dental Implant Process Step by Step

The dental implant journey begins with a thorough diagnostic evaluation. During your complimentary consultation, your surgeon captures a three-dimensional cone beam CT scan of your jaw, which provides detailed images of bone density, nerve locations, and sinus proximity.

This digital scan is used to create a precise surgical plan, often with computer-guided templates that determine the exact angle, depth, and position of each implant for optimal results and minimal invasiveness.

On the day of surgery, local anesthesia or sedation is administered to ensure complete comfort. For single implant cases, the procedure typically takes 30 to 60 minutes.

Full-arch procedures like All-on-4, where four implants support an entire arch of teeth, generally take two to three hours per arch. After the implants are placed, a temporary restoration is attached so you leave the office with functional teeth the same day.

Over the following three to six months, the implants integrate with your jawbone to create a permanent foundation.

The final phase involves replacing your temporary teeth with your permanent custom restoration. At Fusion Dental Implants, our in-house dental laboratory crafts each prosthetic from premium zirconia, a material chosen for its exceptional strength, natural translucency, and stain resistance.

Your permanent teeth are designed to match the shape, shade, and contour of natural teeth, and they are precision-fitted to your implants for a secure, comfortable bite that can last decades with proper care.

Materials and Technology in Modern Implant Dentistry

Modern dental implants are manufactured from medical-grade titanium alloy or zirconia ceramic, both of which are biocompatible and accepted by the human body without rejection.

Titanium has a well-documented 50-year track record in implant dentistry and remains the gold standard for implant posts due to its ability to osseointegrate reliably with jawbone tissue.

The surface of each implant is micro-textured or plasma-sprayed to accelerate bone attachment and improve long-term stability.

The prosthetic teeth attached to implants have evolved significantly from the acrylic restorations of the past. Today, monolithic zirconia is the premium material choice for implant-supported crowns and full-arch bridges.

Zirconia offers superior fracture resistance compared to porcelain, does not chip or stain like acrylic, and can be milled with digital precision to achieve a natural, lifelike appearance.

At Fusion Dental Implants, all full-arch restorations are fabricated from zirconia in our on-site laboratory, which allows us to control quality at every step.

Advanced technology plays a critical role in modern implant treatment. Cone beam computed tomography provides three-dimensional jaw imaging at a fraction of the radiation dose of traditional CT scans.

Digital treatment planning software allows surgeons to virtually place implants before the actual procedure, and surgical guide templates transfer this digital plan to the operating room with sub-millimeter accuracy.

Intraoral scanners capture digital impressions without messy impression materials, improving patient comfort and restoration fit. These technologies combine to make implant procedures safer, faster, and more predictable than ever before.

Long-Term Care and Maintenance of Dental Implants

Caring for dental implants is straightforward and similar to caring for natural teeth. Daily brushing twice a day with a soft-bristled toothbrush and non-abrasive toothpaste removes plaque from the implant surfaces and surrounding gum tissue.

Interdental brushes or a water flosser are recommended for cleaning between implants and under prosthetic bridges where traditional floss may not reach effectively. Antimicrobial mouth rinse can provide additional protection against bacteria that cause peri-implant inflammation.

Professional maintenance visits every six months are essential for long-term implant success. During these appointments, your dental hygienist uses specialized instruments designed for implant surfaces, as metal scalers used on natural teeth can scratch titanium and harbor bacteria.

Your dentist examines the implant, abutment, and restoration for signs of wear, checks the tightness of prosthetic screws, and takes periodic X-rays to monitor bone levels around each implant. Early detection of any changes allows for simple, non-surgical intervention.

While dental implants cannot develop cavities, the surrounding gum tissue is susceptible to a condition called peri-implantitis, which is similar to gum disease around natural teeth. Risk factors include smoking, uncontrolled diabetes, poor oral hygiene, and a history of periodontal disease.

Symptoms to watch for include redness, swelling, or bleeding around the implant site, and any looseness or discomfort should be reported to your dentist immediately.

With consistent home care and regular professional maintenance, dental implants have a documented success rate exceeding 95 percent at the 10-year mark.

Insurance, Financing, and Planning Your Investment

Dental implant costs depend on several factors including the number of implants needed, whether bone grafting is required, the type of prosthetic restoration selected, and the complexity of the individual case.

At Fusion Dental Implants, single tooth implants including the implant post, abutment, and zirconia crown typically range from $1,850 to $5,500. Implant-supported dentures start at approximately $9,999 per arch, and full-arch All-on-4 zirconia restorations begin at $17,999 per arch.

Every estimate is provided in writing during your free consultation with no hidden fees or surprise charges.

Many dental insurance plans now include coverage for implant procedures, particularly PPO plans. Coverage typically ranges from $1,000 to $3,000 per year depending on your specific plan benefits.

Our insurance coordination team verifies your benefits before treatment and helps maximize your coverage.

For patients without insurance or with limited benefits, we offer in-house financing with monthly payments from $60 for single-tooth implants and $250 for All-on-4 full-arch restorations, with terms extending up to 84 months through our healthcare financing partners.

When evaluating the cost of dental implants, it is important to consider the long-term value compared to alternative treatments.

Traditional dentures need to be replaced every five to seven years at a cost of $1,500 to $3,000 each time, and they accelerate jawbone loss which eventually changes facial structure.

Dental bridges require grinding down adjacent healthy teeth and typically last eight to fifteen years before replacement.

Dental implants, by contrast, preserve bone density, protect neighboring teeth, and with proper care can last a lifetime, making them the most cost-effective tooth replacement solution over a 20 to 30 year period.

Your Next Step

Your Next Step Toward a Permanent Smile

Every patient's dental implant journey is unique, and the best way to understand your options is through a personalized evaluation with an experienced implant surgeon. At Fusion Dental Implants, we provide complimentary consultations that include 3D imaging, a detailed treatment plan, and transparent cost estimates so you can make an informed decision about your care.

With four convenient locations across Northern California in Roseville, El Dorado Hills, Folsom, and Rocklin, our board-certified oral surgeons are ready to help you explore whether dental implants are the right solution for restoring your smile, your confidence, and your quality of life. Contact us today to schedule your free consultation.